Phillips

Auction Houses Ask the $16 Billion Question

Sales were through the roof in 2022 but—in the future—who will be the new buyers, how will the houses attract them and what objects will make them spend?

Marion Maneker

5 min read

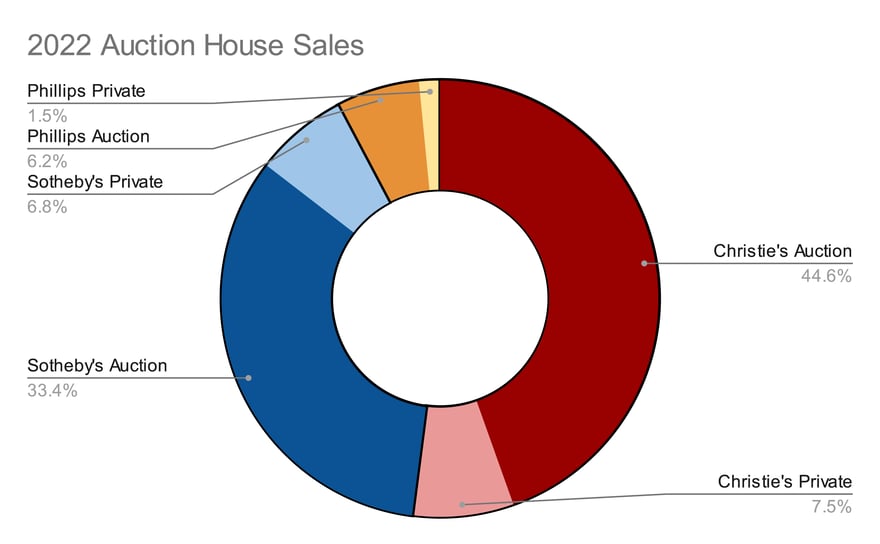

Together, Phillips, Sotheby’s and Christie’s were able to sell more than $16.16 billion in art and luxury goods to buyers around the world. Competitive auctions—in person or online—accounted for $13.6 billion of the art market’s total; and another $2.56 billion was spent in private sales orchestrated by the auction house’s vast network of representatives.

Private sales significantly increased a few years ago but have now stabilized around $1 billion for each of the major houses and $250 million for Phillips. Given Phillips’s small size and reach, the $250 million there is notable for being a much higher percentage of overall sales than at the major houses. Phillips has also seen a 20% rise in private sales volume which is higher than the big houses.

Christie’s edged out Sotheby’s in private sales by around $100 million or less than 10% of the private sales total for each house. Christie’s declared $1.21 billion in private sales for 2022 in its final year-end statement; Sotheby’s said it had sold $1.1 billion.

The big difference in overall results came in auction sales. Christie’s had $7.2 billion to Sotheby’s $5.4 billion. (Sotheby’s had an additional billion in auction sales from vintage cars and its new real estate auction businesses but Christie’s does not have comparable businesses in those areas so we’ve separated that out.) Much of the difference in art and luxury auction sales (but not all of it) comes from the Paul Allen collection which accounted for $1.6 billion in auction sales at Christie’s.

The importance of large collections coming to term was brought home this year. Christie’s was able to sell three of the largest single-owner collections ever to come to auction: Allen, Anne Bass and the Ammann collections. They accounted for nearly a third of Christie’s auction sales. Sotheby’s had its own list of significant collections (Solinger, Hotung and the strong second half of the Macklowe sale) this year, too.

One question that has perturbed the art market has been whether the great works purchased by the generation that is now passing would be of interest—and valued by—the next generation. This year’s auction sales certainly proved that Gen X collectors, those who come after the Baby Boomers and are now reaching their prime earning, wealth and spending years, are up for the task. In their results, the auction houses have turned their attention toward “millennials” who are now interfacing with Sotheby’s and Christie’s primarily through the luxury departments.

Luxury sales—that’s everything that the auction houses sell at auction or privately that’s not art (primarily, but not exclusively, jewelry, watches and handbags)—continue to account for a substantial portion of the overall business. At Christie’s the number was $779 million. Sotheby’s sold $924 million in luxury items.

According to their release, 36% of Christie’s new clients came to the company through luxury sales. At Sotheby’s, half of the bidders in the luxury category were new clients. Now you can see why these relatively small departments are so important. They’re the gateway to bigger ticket purchases. These new clients skew toward the “millennial” age group.

At Christie’s, 21% of all buyers were “millennials.” They also accounted for a third of new clients. Those younger buyers are mostly from Asia. Here’s how Christie’s phrased it [and the emphasis is theirs]: “Of the spend from millennials, in Christie’s global salerooms in 2022, 62% came from millennials in APAC.“

To take it even further, Christie’s revealed in its presentation to the press that millennials spent $110 million with the house, 89% of it digitally. Nearly half of the millennial buyers were from Asia but they spent a full $70 million or close to two-thirds of the total. Clearly, Asian millennials punch above their weight class.

Sotheby’s confirms this trend. Their data shows the client base in Asia expanding with a “record number of bidders, and marked increase in levels of under 40s bidding in Sotheby’s sales (having tripled this year). Asian collectors are spending more per person on average than collectors from elsewhere in the world (just over 20%); and bidding 40% more per person on average. … in Sotheby’s global sales, 68% of new bidders were from countries in Asia.”

Now, here’s where the blizzard of detail gets interesting. Asian buyers were crucial to the success of the art market in 2022. But their participation significantly took place outside of Asia. Part of the reason for this was the global composition of sales. Big collections dominated the year. Those big collections tend to be sold in New York. But Asian buyers showed up there even though the sales volume in the region was down.

Christie’s sales in Asia fell 20% in dollars versus 2021. Getting granular with Christie’s data, we learn that the only category that did not grow last year (between 20/21, Luxury, Classics and Asian & World Art) was Asian & World Art. It too was down 20% in dollars. As demand for art increased, the market for Asian art is contracting. But that doesn’t mean Asian buyers are sitting out. Collectors from APAC bought 29% of the value of the Paul Allen collection, the biggest single-owner art collection ever sold. They spent $460 million! That’s more than the whole Asian and World Art category at Christie’s.

Just to dwell on this for a moment. These numbers outline a real change in taste—at least for now!—among the preponderance of Asian buyers who now seem to want Contemporary art and high-value Modern and Post-war art, the kind you buy in New York (and sometimes London.)

Although the Paul Allen collection represents a substantial portion of Christie’s sales and even of the entire auction market for the year, it only encompasses a small number of lots. Christie’s overall lot count was up in 2022 to 46,322 from 43,386 in 2021. That’s an almost 7% rise in lots. Sotheby’s had even more lots sell. Their count was 59,000 lots sold, a full 28% more than Christie’s.

Perhaps more telling about the overall health of the art market and indicative of future demand, Christie’s sold 85% of the lots that it offered in 2022. Sotheby’s doesn’t track the sell through rate but in the past has reported similar numbers. The 85% figure is historically high. Sell-through rates have been creeping up over the last several years. Last year, Christie’s sell-through rate was slightly higher at 86%

The top line numbers for the art market have risen on the growing sales of superlative collections like Paul Allen’s. But the numbers also show something quite different. Christie’s pointed out that its global sell-through rate was a whopping 85%. This is down slightly from the previous year’s astonishing 86%. But a 1% drop in sell-through to achieve a 7% rise in sold lots isn’t a bad trade off.

Overall sell-through may seem like a wonky statistic—and it is. But it is important in the broader transformation of the auction houses from wholesale businesses to retail ones. In fact, these historically high sell-through rates are a sign that we have reached the end of that transformation. When auctions were a wholesale business, it didn’t really matter how many works failed. In fact, if an auction had too high a sell-through rate the assumption was the auctioneers had not tried hard enough to bring more lots to auction to capitalize on demand.

Over the last decade and a half, we’ve seen sell-through rates rise in the most visible auctions as the houses have become more focused on sale management. But those events only account for a small portion of all the lots offered. A key emphasis for the auction houses—and this applies even more for the luxury categories—is establishing for consumers the idea that objects bought at auction will retain their value.

To achieve this, the vast army of auction house specialists across many different departments have had to become quite adroit at choosing objects to offer that have identifiable buyers and getting consignors to price those works in a way that will achieve the consignors goals but not repel bidders. This has been the hidden transformation of the auction houses that is now bearing fruit in high sell-through rates.

More important for the future, this discipline will become even more central to the auction house’s value proposition as the auction market inevitably goes through a cooling or contracting cycle. The auction market peaked in 2011, 2014, 2018 and 2021. This year was hardly a significant pullback. So logic suggests next year’s sales will be more focused and conservative. In that sort of environment, judgment and skill in assessing the market will become even more determinative of success and failure.